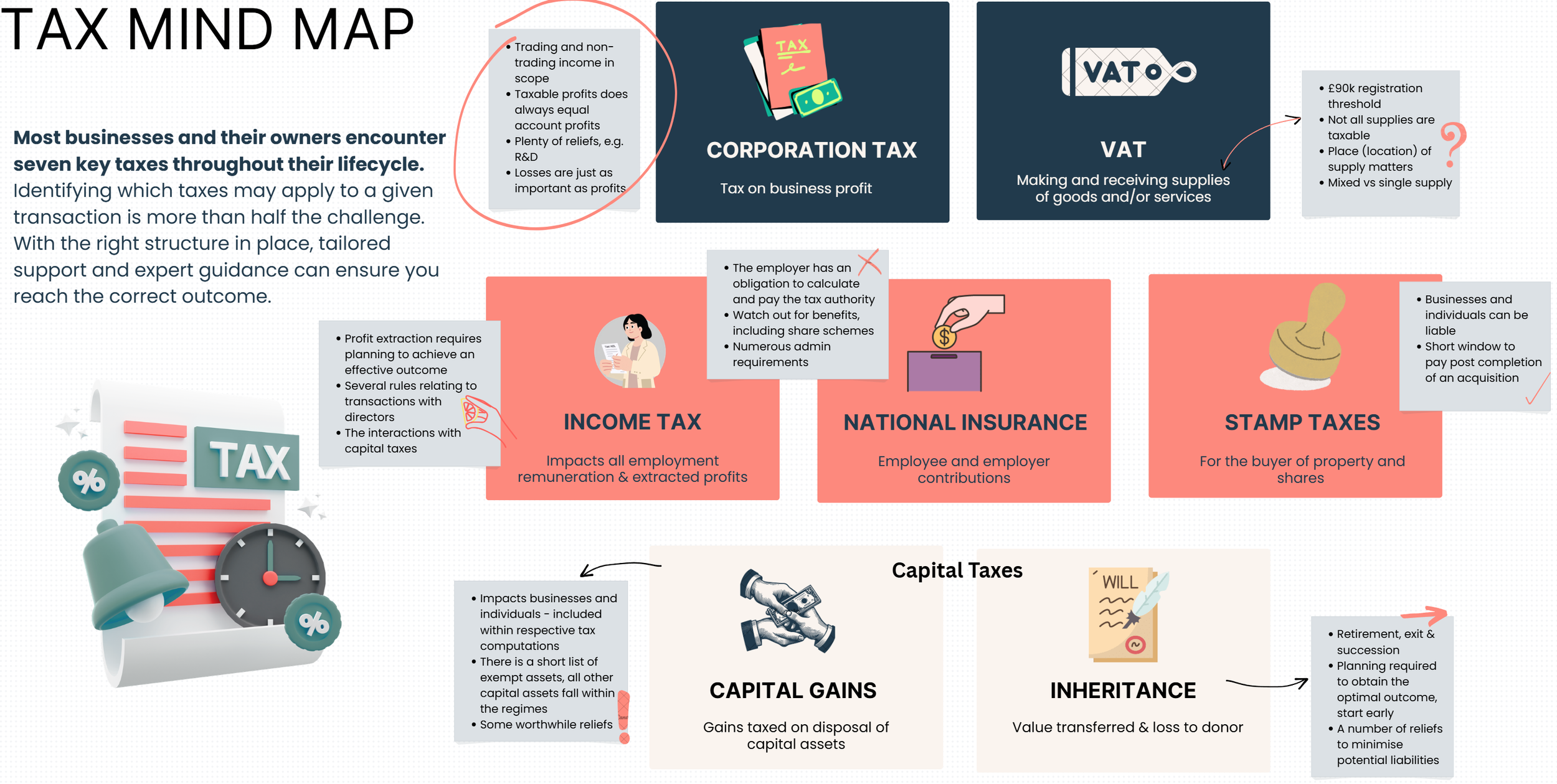

A Tax Map for Businesses

UK businesses and their owners encounter seven core taxes throughout their lifecycle, corporation tax, VAT, income tax, national insurance, stamp taxes, capital gains tax and inheritance tax. Identifying which taxes apply to a given transaction is more than half the challenge. This guide maps out each tax, when it arises and the key planning considerations for businesses and their owners. Written by Ben Leadbetter ACA CTA, Chartered Tax Adviser and founder of The Lumen Collective.

Please note the below content is related to UK taxes. Rates quoted are those enacted in legislation at the time of writing, April 2026.

Taxes often evoke a wince, a sigh or even an expletive, and not just from business leaders. A complex mire of conventions, rules and procedures making many feel lost and frustrated. Everything associated with taxes seems costly and time-consuming. This article attempts to stand back from the mire and create a simple mind map to navigate the complex world of tax.

Most businesses and their owners encounter seven core taxes throughout their lifecycle. Knowing which tax applies to a transaction is more than half the battle. Planning ahead and being aware when taxes might impact your business will move it away from simple compliance to a more strategic approach.

Here’s a breakdown of the seven key taxes and where they commonly arise for most businesses.

Corporation Tax

Tax on business profits. Unfortunately more profits likely means more taxes. And the more variety in business activities means the more nuances in a company’s tax position.

Corporation tax (CT) applies to the trading profits of limited companies, but there are numerous rules about how it’s calculated and when reliefs apply.

Taxable profit ≠ accounting profit – adjustments are needed to accounting profits, for tax-deductible items and non-allowable expenses, to arrive at taxable profits.

Trading and non-trading income – trading (profits), property (rental) and other (e.g. interest) forms of income are all within scope of CT. All forms create taxable profits.

Reliefs - there are numerous reliefs that can help reduce taxable profits. Such as research & development (R&D), annual investment allowance (AIA), chargeable gains reliefs, group and loss reliefs.

Losses - they can be offset against taxable profits from other periods and even group companies. There are several options, a bit of planning and thought is required to achieve the desired result. A balance of cash flow and maximising tax reduction must be considered.

Compliance - stay on the right side of HMRC. There are notification, filing and payment requirements. A simple tax calendar and planning will keep a business up-to-date.

Top tip: Engage in tax planning as early as possible, it can identify significant relief opportunities and avoid nasty surprises.

VAT (Value Added Tax)

Applied on the supply of most goods and services. Adding up to 20% to the price of anything typically grabs attention, and businesses become particularly studious about the detail included on invoices.

VAT can be a complex tax and errors can be common. However the position for most businesses is relatively straightforward as long as they remember some key principles.

£90,000 turnover threshold – Once taxable turnover exceeds £90,000 within any 12-month rolling period, registration is mandatory.

Different rates - Not all supplies are treated equally, there are zero-rated, reduced-rated and exempt. Once a business initially establishes their typical supplies the rates infrequently change. For new transactions or supplies, a bit of research and simple advice will allow the business to adopt the right approach.

Place of supply - the place of supply rules determine where VAT applies and therefore what business is responsible for accounting for the VAT. Similarly to the differing rates, once initially established the rules for place of supply will not change frequently. Be pro-active in discussions with suppliers and customers, they will also want to ensure they adopt the right tax treatment.

Mixed or single supply - often goods and services are bundled together, and more commonly than you might expect the VAT rates for the separate components are different. So it begs the question, do they all get the same VAT rate when supplied together. As you can imagine with VAT, this is not always straightforward, a careful assessment of the contract and substance of the arrangement is needed.

Electronic filing - it is now mandatory for most VAT-registered businesses. HMRC’s making-tax-digital (MTD) approach requires digital record-keeping and compliance submissions. Most accounting and tax software have built automatic connections with HMRC to meet the MTD requirements.

Top tip: Invest in regular advice when conducting new transactions, supplies and contracts. The potential tax savings and avoidance of penalties are often significant. Use digital automation tools for compliance.

Income Tax

For Companies:

Affects all employee remuneration and benefits. Almost ubiquitous in its impact on taxpayers, it dwarfs all other taxes in terms of government receipts. As a result it is comparatively well dealt with by taxpayers.

While employees pay income tax via PAYE, the business has strict obligations as the employer.

PAYE and Real Time Information (RTI) Reporting – the employer is obliged to calculate the PAYE liability and withhold the taxes, report and pay to HMRC each month. Tax codes are used to calculate the tax owed, submissions can be made via HMRC’s website but typically payroll or accounting service providers have their own integrations.

Benefits in kind – these include benefits such as company cars, medical insurance, gym memberships etc. From 6th April 2026, all benefits will need to be included within monthly payroll calculations, so employers must calculate and include in each month the cash equivalent value of any benefits provided to employees.

Director remuneration – salary and dividend are treated as different types of income and therefore different tax treatments are adopted. Dividend income is not included within PAYE income, it is taxed separately via the self assessment process.

Expenses policies – employees can be reimbursed in full without the payments being taxed as income if the expenses were ‘wholly, exclusively and necessarily’ for the purposes of the trade. The definition of ‘wholly, exclusively and necessarily’ can be a little tricky to pin down, but some research and where needed some advice will guide employers in the right direction.

Top tip: Work with benefit providers to understand the value of benefits, they will likely have come across the issue before. Some independent research and consulting HMRC’s guidance will go a long way to making the right decisions. Where it is a little more complex, seek some professional advice, the work and cost will be worth it for peace of mind and avoiding penalties.

For Individuals (owners):

Extracted profits. Owner-managers face additional complexity as they are both director and shareholder, with different tax treatments applying to each role.

Profit extraction – salary, dividends, pension contributions and other forms of remuneration each carry different tax and NIC consequences. A blended approach, reviewed annually, will almost always produce a better result than a fixed salary and dividend split.

Transactions with directors – loans to directors can attract a tax charge equivalent to the dividend income tax, if not repaid within nine months of the year end. Benefits provided to directors must be reported and payments to connected persons must be commercially justifiable to be deductible.

Interaction with capital taxes – decisions on remuneration and retained profits interact with capital gains tax on a future exit and inheritance tax on succession. Income tax planning for owner-managers should never be done in isolation from the broader tax position.

Top tip: A set-and-forget approach would be great, yet tax legislation is always changing and such an approach can easily become inefficient, or worse problematic. Review your profit extraction strategy before the start of each tax year. A joined-up review across income tax, corporation tax, capital gains and pensions. Consistent reviews and marginal changes will make a significant difference in the long run.

National Insurance

Contributions from both the business and the employee. National insurance contributions (NICs) enable entitlement to certain social security benefits (e.g. the state pension, maternity / paternity, statutory sick pay). Often contributions are overlooked as they are lumped in within income tax. But the contributions are not as pervasive as income tax, there are distinct rules and costs to businesses (and employees). There are certain forms of income outside of the scope of NICs.

Employers have the obligation to pay their own and their employees’ NICs, typically as part of the PAYE and RTI framework.

Employer’sNICs - up to 15% is due on the gross salary and bonus costs of each employee. There are threshold limits depending on the level of wage / salary.

Directors -the treatment can differ as directors may not be paid on regular intervals like employees. If so, the NIC liabilities are calculated on a cumulative basis throughout the year.

Class 1A NIC – payable on a variety of employee benefits. The contributions will be due each month as part of the PAYE and RTI framework, as all benefits bar a select few exceptions must be included in periodic payroll processes, rather than a year-end procedure.

Reliefs – such as the Employment Allowance (up to £10,500 pa). There is eligibility criteria to be met, although most businesses should qualify. HMRC guidance and most payroll providers make obtaining reliefs a straightforward process.

Top tip: Payroll providers and software are very well versed at calculating NIC liabilities. The key task for businesses is to ensure the input data is accurate, such as salaries, employment type (directors) and value of benefits.

Stamp Taxes

Tax on property and share purchases. Normally first encountered by taxpayers when purchasing a first home, it can be quite a shock as the tax liability can be significant. As property and share transactions become more complex so do the rules for stamp taxes, even hardened tax advisers can winch at the nuances involved.

Stamp duty applies in specific, often high-value, property and share transactions. Always paid by the purchaser, shares and property.

Stamp Duty Land Tax (SDLT) – charged on the completion (not exchange) for commercial or residential property. There are differing rates and brackets for commercial and residential properties, with commercial rates being lower. Be mindful that consideration includes VAT, as well as inclusion of contingent, uncertain or unascertained consideration.

Stamp Duty on shares – applies to private share transfers. A 0.5% (sometimes 1.5%) tax is levied on the share transfer value, but only if the consideration exceeds £1,000. There are also some exemptions on the type of instrument (e.g. units in an ETF) and upon certain events (between group companies). For a share transfer to be formally registered it must be officially ‘stamped’. Consideration can be cash, share or debts.

Short payment window – for shares there is a 30 days window from the date of the transaction. For land transactions, the window is shortened to 14 days post completion.

Corporate transactions – partnerships, incorporations, group restructurings or M&A transactions all have nuances and exemptions to consider.

Top tip: For any significant property and share transactions have a mindset that stamp taxes will apply. Seek advice on mixed use properties, potentially linked property transactions, restructuring and M&A activity. Changes to steps and papering of transactions can mean a significantly lower tax liability.

Capital Gains Tax (CGT)

Charged on the profit from selling assets. Often perceived as a tax on wealth and impacting a select few businesses and individuals, yet as businesses engage in ever more varied activity and individuals hold more business assets the application of CGT is growing.

There are capital gains regimes for individuals and companies. It may impact a business owner in both a personal capacity, as they sell shares or assets, as well as within a company structure.

For Companies (Chargeable Gains Regime):

Corporation tax - chargeable gains are calculated similarly to individuals, as noted above, proceeds less cost and incidental costs. The chargeable gain is included within a business’ taxable profits.

Tax rates - as any gains are included in taxable profits they are taxed at the applicable corporation tax rate for the company.

Reliefs - there are fewer types of relief. However gains can often be exempt when selling a significant shareholding, such as that in a subsidiary, via the Substantial Shareholding Exemption (SSE). Deferral reliefs are also available to rollover gains to a future disposal event when proceeds are re-invested in new business assets.

Capital losses - can offset future chargeable gains. However capital losses cannot be offset against trading or other profits.

Top tip: Disposal of capital assets will bring about taxable events, but also numerous opportunities to gain relief. The calculations and criteria can be a little complex but applying the basic rules can materially reduce tax liabilities.

For Individuals (Owners):

Asset disposals in scope - Applies to disposals of numerous assets shares, land, property, crypto, goodwill and IP. The legislation lists exempt assets rather than including specific assets that fall within the regime.

Reliefs:

Begins with an annual exempt amount, which is £3,000.

Tax reducing reliefs, that can reduce the CGT rate to 18%, on disposal of qualifying assets and criteria. Such as Business Asset Disposal Relief (BADR). Principal private residence (PPR) relief can exempt gains on an individual’s main and private residence. On death, the CGT base cost of assets is uplifted to market value, so no capital gain arises on the transfer to beneficiaries.

Deferral reliefs, such as gift and rollover reliefs that can move the CGT liability to a future event. Inter-spouse transfers are at ‘no gain no loss’, so no tax is charged until a disposal is made to a third party.

Incidental costs of disposal such as legal fees and advertising are deductible, as are associated costs of acquisition such as legal fees and stamp duty land tax.

Numerous rates - there are differing rates for lower and higher income tax payers. As well as residential property which have higher rates.

Timing matters – it is very important in exit or succession planning. As well as significant events such as incorporating a business.

Administration - gains on residential properties must be reported and the tax paid within 60 days of completion. Other gains can be reported and paid as part of the self assessment return.

Top tip: There are significant interactions with inheritance tax (IHT), so make sure both taxes are considered together when disposing of capital assets.

Inheritance Tax (IHT)

Applies on transfers of value and wealth succession. Sometimes referred to as a ‘death tax’, which is a little sobering. Business leaders will want to know how the assets they have worked so hard to accumulate during their lifetime are dealt with as they seek to pass them on to the next generation.

For business owners, their wealth is often largely invested within their business. Extracting, transferring or realising this value should initiate IHT (and CGT) planning, especially where succession is a goal.

Value transferred – IHT transfers are measured on the basis of the loss to the donor’s estate. Related property, typically owned by a spouse, needs to be considered. Transfers at death and in the 7 years prior are considered within the IHT calculation. Transferred value is subject to a 40% tax rate, after applying certain reliefs.

Reliefs:

Nil rate bands - up to £325k of transferred value is not charged to tax. It is commonly known, but there are nuances. Including a more recent additional ‘private residence nil rate band’, which allows for additional nil rate band if there is a private residence in the death estate being passed to lineal descendants.

Annual exemption of £3,000 which can be carried forward one tax year, if unused.

Inter-spouse transfers - gifts to spouses are exempt, and unused nil rate bands can also be transferred on death.

Business Property Relief (BPR) – certain transferred business assets, typically a trading company or assets of a trading company, are partially exempt from IHT. Agricultural Property Relief (APR) works in a similar way for agricultural assets. There are caps on the level of exemption for BPR and APR, so it’s important to stay up-to-date with the latest legislation.

Interaction with CGT - CGT and IHT are known as the ‘capital taxes’, each should be considered when disposing of business property. Timing and events could trigger one or both, so planning for a desired outcome is key.

Top tip: Ownership structure and shareholder agreements can impact relief eligibility, review these periodically with tax and legal advisers.

Conclusion: From Complexity to Clarity

A mind map of the relevant taxes creates awareness. Using this awareness, with some basic research with modern tools, can make you much more informed. There are complexities, continual legislative changes, the importance of timing and understanding business (and personal) context mean getting advice early where needed will be beneficial. The results will speak for themselves.

Plan proactively for growth, changes, sales or succession.

Avoid penalties and errors.

Unlock cash savings and reliefs.

FAQ Section

What are the main taxes a UK business needs to consider?

Most UK businesses encounter seven core taxes: corporation tax on trading profits, VAT on supplies of goods and services, income tax and national insurance on employee remuneration, stamp taxes on property and share purchases, capital gains tax on asset disposals, and inheritance tax on transfers of value. The relevance of each depends on the nature and stage of the business.

When should a business start tax planning?

As early as possible. Tax planning before transactions, restructurings or significant business changes can identify relief opportunities and avoid costly surprises. Reactive tax work after the event is almost always more expensive and less effective.

Do I need a Chartered Tax Adviser or can my accountant handle tax?

Many accountants handle routine compliance well but may lack depth in specialist areas such as corporate restructurings, international tax, capital gains planning or VAT on complex supplies. A Chartered Tax Adviser (CTA) holds the highest UK tax qualification and is trained across all major tax types. For businesses with growing complexity, engaging a CTA alongside your accountant can add significant value.

How do corporation tax and capital gains tax interact?

For companies, chargeable gains are included within taxable profits and taxed at the corporation tax rate. For individual shareholders, capital gains on share disposals are taxed separately under the CGT regime, with different rates and reliefs available. Business owners should consider both regimes together, particularly when planning exits or restructurings.

Learn more about our tax advisory services.

Disclaimer:

The information provided in this blog post is for general information purposes only and does not constitute tax, legal, or financial advice. It should not be relied upon for making decisions or taking any action. Tax laws and regulations change regularly and may vary depending on your specific circumstances. You should seek appropriate professional advice from a qualified tax adviser before acting on any of the information contained herein.